Key Takeaways

- The amount you can borrow from a licensed money lender in Singapore depends mainly on your annual income, residency status, and whether the loan is secured or unsecured.

- Unsecured loan limits in Singapore are regulated by law and apply to all licensed money lenders, not just a single lender.

- Even if you qualify for the maximum borrowing limit, lenders will still assess your repayment capacity, credit history, and existing debts before approving the final loan amount.

- Borrowing from a licensed money lender is regulated and safer than dealing with a private, unlicensed money lender, which often involves a slew of illegal practices and hidden risks.

- Always borrow only what you need and carefully review interest rates, fees, and repayment terms before signing any money loan in Singapore.

Need extra cash but not sure how much a licensed money lender can legally lend you in Singapore?

Whether you’re planning to cover an unexpected expense, pay for a major purchase, or bridge a temporary cash flow gap, understanding your borrowing limit is an important first step. Unlike borrowing from an unlicensed money lender, borrowing from a licensed money lender in Singapore is regulated by law, with clear rules that protect borrowers from excessive fees, unfair practices, and irresponsible lending.

That being said, many borrowers are surprised to learn that the amount they can borrow is not entirely up to them. Even though there are legal limits, lenders also carefully assess your ability to repay before approving any loan.

Intrigued? Here’s what you need to know before applying for a money loan in Singapore.

What Is a Licensed Money Lender in Singapore?

A licensed money lender in Singapore is a lender approved and regulated by Singapore’s Ministry of Law. Every licensed money lender must comply with regulations governing loan contracts, interest rates, late payment fees, advertising practices, and debt collection procedures.

These rules help ensure that borrowers are treated fairly throughout the loan process. For example, there are caps on the interest rate a licensed money lender can charge, as well as restrictions on the fees lenders can impose.

This is very different from dealing with an unlicensed money lender, who often engages in illegal practices such as harassment, hidden charges, exorbitant interest rates, intimidation, and unsolicited loan offers via WhatsApp, SMS, or social media.

Before applying for any loan, always verify the lender’s legitimacy; ensure the lender appears on the official Registry of Moneylenders’ list of lenders. This is one of the simplest ways to confirm that you are dealing with a legal money lender and not an illegal operator.

How Much Can I Borrow From a Money Lender?

One of the most common questions borrowers ask is, “How much can I borrow from money lender companies in Singapore?”

The answer depends primarily on your annual income and residency status. Singapore regulations set borrowing limits for unsecured loans, which do not require collateral.

It is important to note that these limits apply to the total amount you owe across all licensed money lenders combined, not just a single lender.

For secured loans, the borrowing amount is generally determined by the value of the collateral pledged rather than your annual income.

Borrowing Limits for Singapore Citizens, Permanent Residents, and Foreigners Residing in Singapore

| Annual Income | Singapore Citizens & Permanent Residents | Foreigners Residing in Singapore |

|---|---|---|

| Less than S$10,000 | Up to S$3,000 | Up to S$500 |

| At least S$10,000 but less than S$20,000 | Up to S$3,000 | |

| At least S$20,000 | Up to 6X monthly income | |

These limits represent the maximum unsecured loan limit that Singapore regulations allow licensed lenders to grant.

For example, if you earn S$3,500 per month and your annual income exceeds S$20,000, your maximum borrowing limit for unsecured loans may be up to six times your monthly income, subject to lender approval.

If you’re researching a personal loan, how much you can borrow is often one of the first questions you’ll have. While the legal limits provide a useful guideline, they do not automatically determine how much you will actually receive.

If I Fulfil the Minimum Income Requirement, Can I Borrow Up to My Legal Limit?

Not necessarily.

Although income is an important factor, it is only one part of the assessment process. A licensed money lender will also evaluate your overall financial situation before determining the final loan amount.

Some factors lenders may consider include:

- Your existing debt obligations

- Your monthly repayment commitments

- Your employment and income stability

- Your repayment history

- Information obtained from the Moneylenders Credit Bureau (MLCB) loan information report

For instance, even if you qualify for the maximum borrowing limit based on your income, a lender may approve a smaller amount if they believe a higher loan would place excessive strain on your finances.

Why is due diligence crucial? This approach helps promote responsible borrowing and reduces the risk of financial difficulties later on.

Instead of focusing solely on the highest amount available, consider how much you genuinely need and whether the repayments comfortably fit within your monthly budget. Borrowing more than necessary can increase your financial burden without providing any additional real benefit.

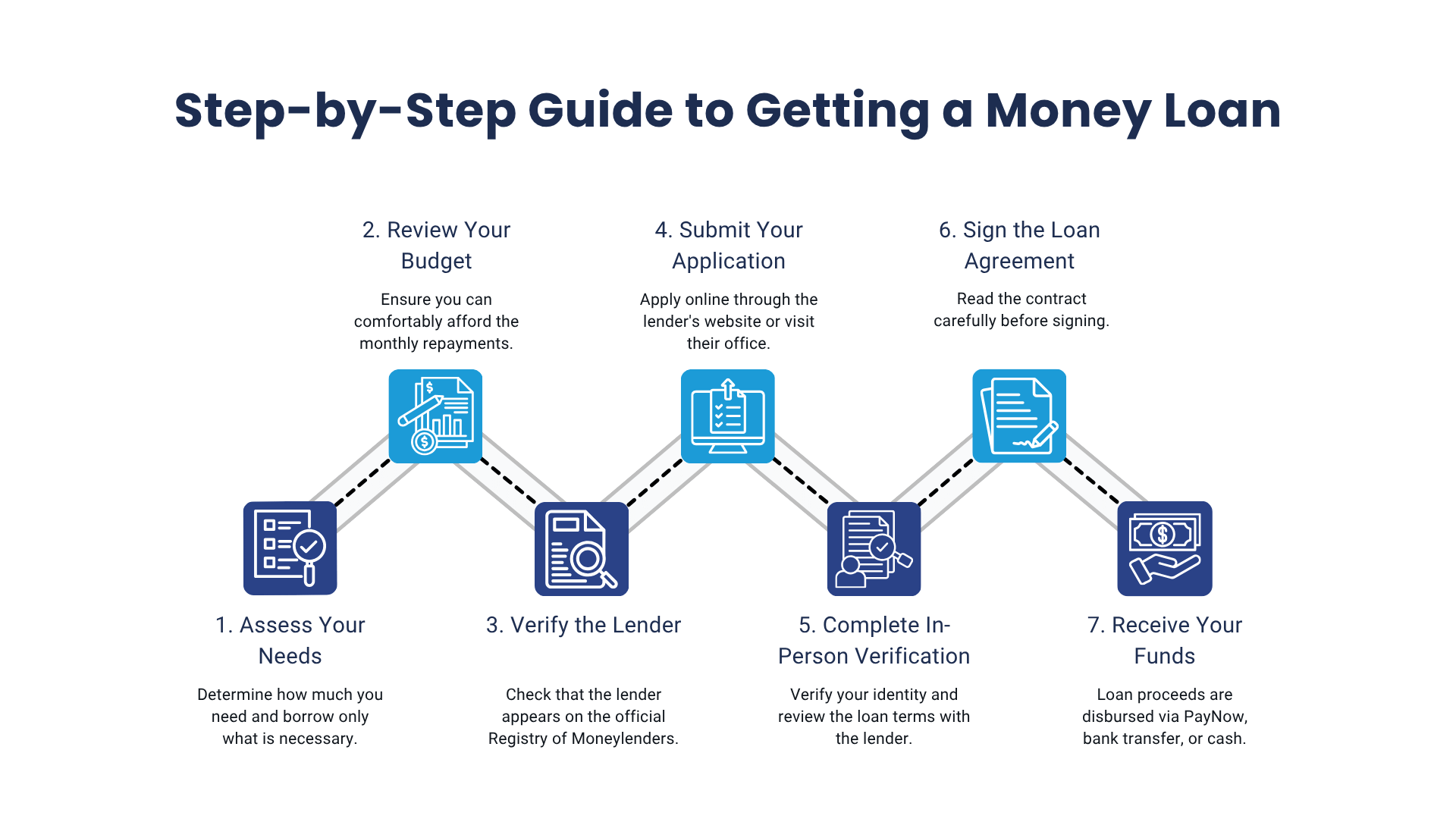

How to Apply for a Money Loan in Singapore Safely

If you’re considering a money loan in Singapore, following a structured application process can help you borrow responsibly and avoid unnecessary risks.

UK Credit offers several loan options to suit different borrowing needs and guides applicants through every step of the process, helping you to make informed borrowing decisions with confidence.

Conclusion

The amount you can borrow from a licensed money lender depends on several factors, including your annual income, residency status, and whether the loan is secured or unsecured. While Singapore’s regulations establish clear borrowing limits, the final approved amount is determined by a broader assessment of your financial situation, not just your income.

Understanding these limits can help you make informed borrowing decisions, but the maximum allowable amount should never be viewed as the ideal amount to borrow. As it stands, responsible borrowing means taking only what you need and ensuring you can comfortably manage the repayments at the same time.

Before signing any loan agreement, always review the interest rates, fees, repayment schedule, and terms carefully so you know exactly what you are committing to.

If you are unsure how much you can borrow, speak with UK Credit for a clear, no-obligation discussion. As a dependable licensed money lender in Singapore that’s earned the trust of the community, UK Credit can help you understand your loan options, repayment terms, and borrowing limits before you apply for a loan.