Key Takeaways

- A credit score in Singapore is a numerical indicator of a borrower’s creditworthiness, calculated by Credit Bureau Singapore (CBS) based on factors such as repayment history, outstanding debts, and recent credit applications.

- CBS assigns credit scores ranging from 1,000 to 2,000, with higher scores generally indicating lower repayment risk and potentially improving a borrower’s chances of securing loans or credit facilities on favourable terms.

- A credit report in Singapore provides a detailed record of an individual’s borrowing behaviour, including loan accounts, repayment history, outstanding balances, and credit enquiries, which lenders may review during credit assessments.

- Factors such as late repayments, high credit utilisation, multiple credit applications within a short period, and serious negative records like defaults or bankruptcy may negatively affect a person’s credit score, although improvement is possible through consistent financial discipline.

- Borrowers with a bad credit score may still qualify for financing through licensed money lenders, as they often consider additional factors such as income stability and repayment capacity rather than relying solely on credit scores.

Your credit score plays an important role in your financial journey in Singapore. Whether you are applying for a credit card, personal loan, or housing loan, banks and financial institutions review your credit history to assess how likely you are to repay your debts on time before determining whether to approve the credit facility.

But does having a low credit score automatically mean you cannot get a loan? Not necessarily. There are legal financing options available from Singapore licensed money lenders.

While a poor credit history may reduce your borrowing options, there are ways to improve your credit standing over time. Understanding how your credit score works is the first step towards making informed borrowing decisions and strengthening your overall financial health. Ready to learn more? Let’s dive in!

What Is a Credit Score?

A credit score is a numerical representation of a borrower’s creditworthiness. In Singapore, this score is issued by the Credit Bureau Singapore (CBS) and is commonly referred to as a credit bureau score.

Your credit score in Singapore is calculated based on your borrowing behaviour, including repayment history, outstanding debts, and recent credit applications. A higher credit bureau score generally suggests to lenders that you’re a more reliable borrower as you pose a lower repayment risk. On the contrary, a lower credit bureau score signals a higher likelihood of default—in their eyes, a less desirable borrower.

Banks and financial institutions often refer to CBS records when assessing loan or credit card applications. Although a strong credit bureau score does not guarantee approval, it may improve your chances of obtaining financing on favourable terms.

What Is a Good Credit Score In Singapore?

Understanding Good and Bad Credit Score Ranges

Many borrowers wonder, “What is a good credit score?” In Singapore, credit bureau scores range from 1,000 to 2,000.

Generally, a higher score indicates a lower probability of default, while a lower score suggests a higher probability of default. These scores are grouped into risk grades:

- AA: 1,911 to 2,000 (lowest risk of default)

- BB to GG: 1,724 to 1,910 (intermediate risk levels)

- HH: 1,000 to 1,723 (highest risk of default)

Some individuals may receive a CX rating instead of a numerical score. This usually indicates insufficient credit history rather than poor financial behaviour. Fresh graduates, first-time borrowers, and expatriates who are new to Singapore commonly receive this rating.

During the credit assessment process, lenders may interpret different score bands differently. As it stands, borrowers with higher scores may enjoy better borrowing terms, while those with lower scores inevitably face stricter assessments and enjoy less competitive terms.

What Is Considered a Bad Credit Score?

A bad credit score generally refers to a score that falls within the lower risk bands, particularly those associated with a higher likelihood of default.

A bad credit score may make it more difficult to obtain bank loans, credit cards, or other financing products. For instance, applying for a credit card with a bad credit score in Singapore may result in additional requirements or rejection.

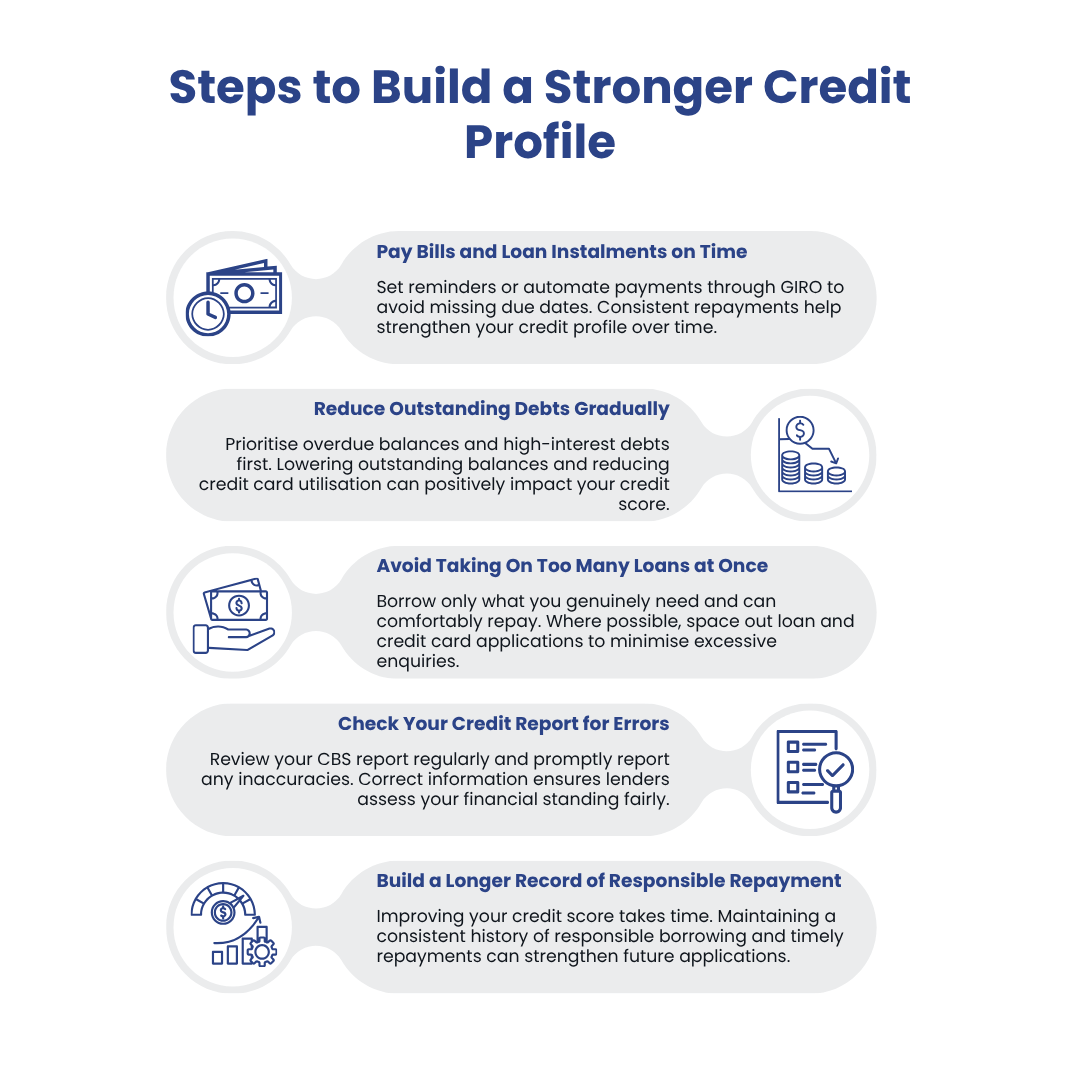

That being said, a bad credit score is not permanent. Consistently making repayments on time and practising responsible borrowing habits can gradually improve your CBS report’s credit standing.

What Is a Credit Report In Singapore?

A credit report Singapore borrowers obtain from CBS provides a detailed overview of their borrowing history and financial behaviour.

A typical CBS report may include:

- Existing and past loan accounts and credit facilities

- Credit card accounts

- Repayment history

- Outstanding balances

- Recent credit enquiries

- Records of overdue payments or defaults, if applicable

- Bankruptcy proceedings or bankruptcy-related records, if applicable

Lenders use this information to better understand a borrower’s credit behaviour, repayment track record, and overall credit risk before making lending decisions.

Key data retention periods within a CBS report may include:

- Repayment history is generally displayed on a rolling 12-month basis.

- Credit enquiry records are typically retained for up to two years.

- Bankruptcy records may remain on file for five years from the date of official discharge.

It is important to note that a credit report serves as a historical snapshot of a borrower’s financial behaviour. It does not determine whether a loan application will be approved.

CBS Report Vs Credit Score

Although the terms are often used interchangeably, they are different.

A CBS report is a detailed record of your credit information and borrowing history.

A credit score, on the other hand, is the summary number and risk indicator derived from the information contained within the CBS report.

Both the CBS report and credit score may influence how lenders evaluate a borrower’s application. This is particularly true if you’re borrowing from traditional banks and financial institutions.

How to Check My Credit Score in Singapore

Where Can You Check Your Credit Score?

If you are wondering how to check your credit score, Singapore consumers can do so by purchasing their CBS report directly from Credit Bureau Singapore for a small fee of S$8 before GST.

Checking your credit report helps you understand your current financial standing before applying for a new loan or credit card. This can help you identify areas for improvement and avoid unnecessary application rejections.

It is also advisable to review your CBS report regularly for outdated, inaccurate, or unfamiliar information. Promptly reporting discrepancies helps ensure that your records remain accurate.

Importantly, obtaining your own CBS report is considered a self-enquiry and does not lower your credit score.

What Affects Your Credit Score?

Late Or Missed Repayments

Repayment history is one of the most significant factors affecting your credit score in Singapore.

Repeated late payments on credit cards, personal loans, and instalment plans may negatively impact future borrowing applications. Consistently missed payments may also signal financial distress to lenders.

We can’t stress enough on the importance of making repayments on time, which remains one of the most effective ways to maintain a healthy credit profile.

Credit Utilisation

Credit utilisation refers to the amount of available credit you are currently using.

For example, if your total credit limit is S$10,000 and you have utilised S$8,000, your credit utilisation ratio is 80%.

High utilisation may suggest that you are heavily reliant on borrowed funds, which could affect your chances of securing new financing or lead to stricter lending terms.

Where possible, borrowers should aim to keep their credit utilisation below approximately 30% of their available credit limits to improve their chances of loan approval from banks.

New Credit Applications

Applying for multiple loans or credit cards within a short period may indicate higher credit risk.

Each new application creates a hard inquiry, which may affect your credit score. Frequent applications may therefore reduce your chances of approval.

Remember, checking your own CBS report only creates a soft enquiry and does not affect your credit score!

Defaults, Bankruptcy, Or Debt Collection Records

Serious negative records, such as loan defaults, bankruptcy, or debt collection activity, may affect your creditworthiness for a longer period.

These records may weaken your chances of obtaining new financing, particularly from banks and financial institutions.

Nevertheless, financial setbacks do not define your future. With consistent repayment and responsible financial management, it is possible to rebuild your credit profile over time.

How to Improve Your Credit Score in Singapore

Can You Get a Loan With a Bad Credit Score?

Yes, it is still possible to obtain a loan with a bad credit score, although approval from banks may be more challenging.

Banks typically place significant emphasis on a borrower’s credit history and may impose stricter eligibility criteria for applicants with weaker credit profiles.

However, borrowers seeking a personal loan with a bad credit score may have a better chance with licensed money lenders. Unlike banks, licensed lenders typically consider additional factors, such as income stability, employment status, and overall repayment history, when assessing applications.

As a result, borrowers with lower credit scores may still qualify for financing, provided they demonstrate adequate ability to repay the loan responsibly.

Related read: Guide to Money Lenders vs Banks: Who Should You Borrow From?

Are No Credit Check Loans Real in Singapore?

No, there are no genuine, legal “no credit check loans” in Singapore.

All legitimate lenders are required to assess a borrower’s ability to repay before approving a loan. While banks typically rely heavily on credit scores, licensed money lenders do not assess them in the same way.

Instead, licensed money lenders generally review the borrower’s Moneylenders Credit Bureau (MLCB) report alongside other financial information to assess creditworthiness.

Borrowers should remain cautious of lenders advertising guaranteed approvals or claiming that absolutely no checks are required, as such claims may be warning signs of illegal lending activities.

Conclusion

A credit score is an important measure of your creditworthiness and plays a significant role in many borrowing decisions in Singapore. Although a bad credit score may limit your financing options, it does not have to remain that way permanently. Through consistent repayments, responsible borrowing, diligence, and regular monitoring of your credit report, you can gradually improve your financial standing.

If you require financing despite having a poor credit history, consider approaching a licensed money lender and avoid illegal lenders at all costs. At UK Credit, we provide transparent loan terms and personalised assessments to help borrowers find suitable financing solutions. Contact us today or apply online to explore your options.