Key Takeaways

- You may still obtain a personal loan without a payslip. What matters is demonstrating that you can manage repayments even without a standard salary slip.

- Alternative documents may be valid, too. Bank statements, CPF contribution history, IRAS Notices of Assessment, contracts, invoices, or business records can support your application.

- Legal borrowing caps still apply. Even without a payslip, unsecured loan limits are determined based on your recent income, typically averaged over the 3 months before your application.

- Licensed money lenders must adhere to strict legal limits. Interest, late interest, fees, and total loan costs are capped to protect borrowers and ensure transparency.

- Always verify the lender before applying. Take a few minutes to check MinLaw’s official list of licensed money lenders and avoid lenders that offer “100% online” loans.

Unforeseen expenses have a way of showing up at the worst possible time. If you don’t have a payslip or standard proof of income on hand, the situation can feel even more stressful. Hence, it’s no surprise that many people start searching things like “personal loan without payslip”, “loan in Singapore without payslip”, or “personal loan without income proof” on the internet.

This is often the case for freelancers, self-employed individuals and gig workers. You might still be earning an income, just not in a way that fits the typical paperwork requirements of traditional banks. And if you’re seeking a loan with a less-than-perfect credit history, it can feel even more uncertain trying to figure out your options for a personal loan with bad credit.

In this guide, we’ll walk you through what’s actually possible when it comes to getting a personal loan without income proof in Singapore from licensed money lenders.

Can You Get a Personal Loan Without a Payslip in Singapore?

Yes, it is possible—but you will still need to show proof of income in other ways, such as your Singpass MyInfo records, IRAS Notices of Assessment (NOA), CPF contribution history, bank statements, or invoices. Such documents provide lenders with a clearer picture of your repayment ability and suitability for a personal loan without traditional income proof in Singapore.

In other words, it’s impossible to get a legal loan without any form of income proof.

Beware of Illegal “No Income Proof Loans” in Singapore

Ads promising “personal loans without documents”, “no income proof loans in Singapore”, or “loans without income” should set off some alarm bells in your head. All licensed lenders in Singapore are legally required to check your income and loan eligibility—there are absolutely no exceptions.

Be very cautious of unsolicited loan offers received via social media, WhatsApp/Telegram, or SMS from self-proclaimed “money lenders without payslips”: more often than not, these are illegal or scam operators out to prey on vulnerable borrowers. Claims of instant or fully online loan approvals are also a sure sign of illegal lending activity.

To stay safe, always confirm that the lender is listed on MinLaw’s official list of licensed lenders. If a loan offer feels suspicious, it’s best to walk away immediately.

Who Might Consider a Loan Without Standard Income Proof?

For many borrowers, the challenge isn’t that they don’t earn enough—it’s that their income isn’t reflected in a traditional payslip, which is compulsory for most bank loan applications. Licensed lenders, on the other hand, have adapted to the changing workforce and can accept a wider range of documents to verify income and repayment ability, giving non-traditional earners access to personal loans even without traditional documents.

Self-Employed Individuals

Freelancers, small business owners, and gig workers often don’t receive monthly payslips; instead, their earnings are usually documented through bank statements, invoices, business transaction records, or IRAS Notices of Assessment. Most licensed lenders accept these records as proof of repayment ability.

Commission-Based or Contract Workers

Workers with variable pay—such as sales staff, delivery riders, Grab drivers, or contract employees—receive income based on completed tasks or commissions. In this case, the focus is on demonstrating consistent cash flow rather than a fixed monthly salary.

Newly Employed or Fresh Graduates

Borrowers who have recently started a new job but have not received their first payslip yet may find it difficult to secure a loan from conventional banks. In such cases, lenders may accept Letters of Appointment or Employment Contracts as proof of expected income.

How Licensed Money Lenders Assess Loan Applications

As mentioned above, it is possible to get a loan in Singapore without payslips, but not without any income assessments. So, how exactly do licensed lenders assess your suitability for a loan?

There are a few areas that they look at: first, your income stability—whether your earnings, even if irregular, are consistent enough to support your monthly repayments on top of your daily expenses. The next thing they’d check would be your existing debt obligations, which can be found in your Moneylenders Credit Bureau (MLCB) report, to ensure you do not exceed the legal borrowing limit.

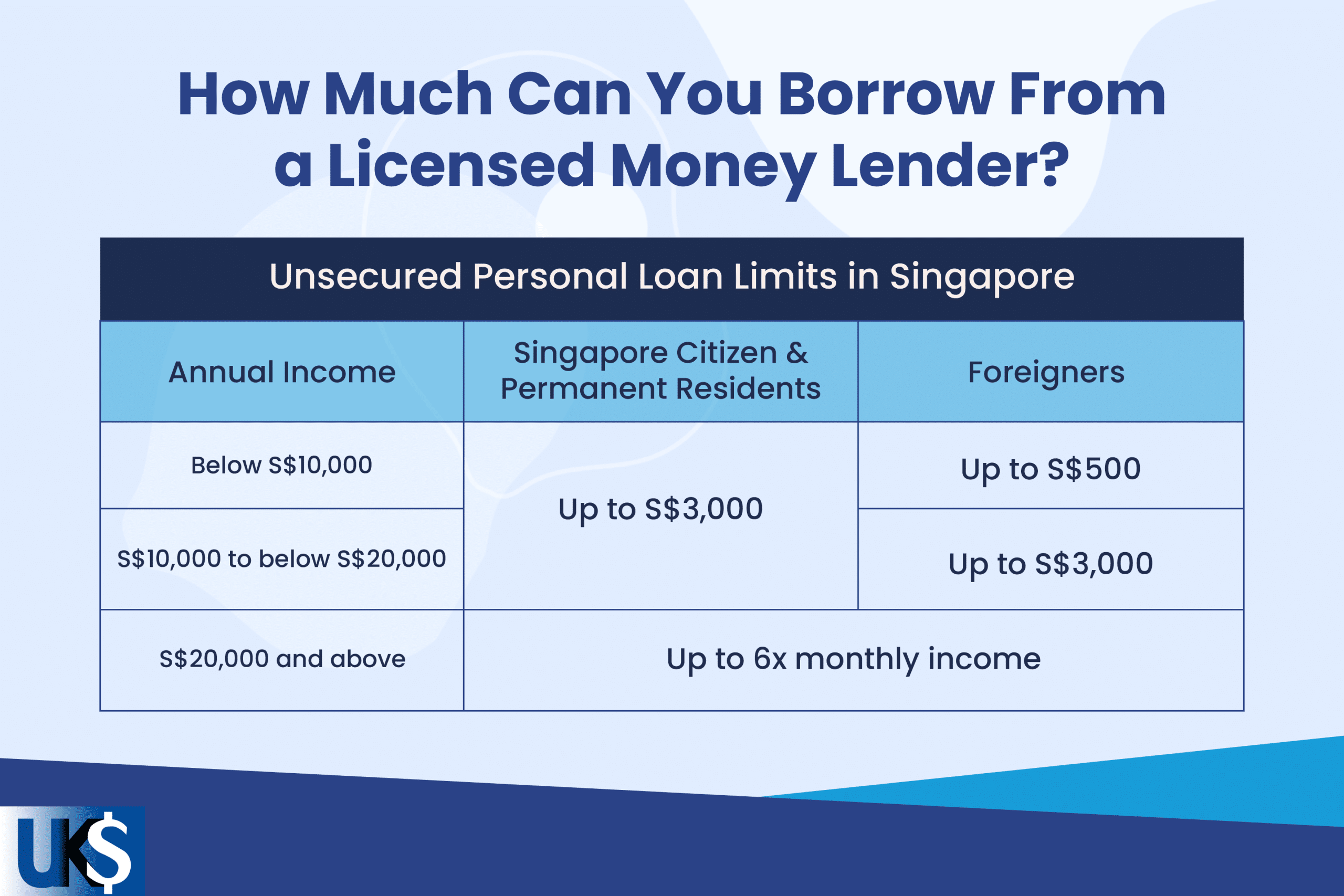

Borrowing Limits for Personal Loans in Singapore

Even if you’re applying for a personal loan without a payslip, there are clear limits on how much you can borrow from licensed lenders within the boundaries of the law:

Regardless of your loan amount, borrowers in Singapore are protected by strict caps on borrowing costs. Licensed lenders can charge up to 4% per month in interest, with late interest capped at 4% per month on overdue amounts only. Late fees cannot go beyond S$60 per month, and administrative fees are strictly capped at 10% of the principal (deducted directly upon approval).

Tips to Boost Your Approval Chances Without a Payslip

If you have irregular income but would like to apply for a loan in Singapore without standard payslips, here’s how you can improve your chances:

#1 Prepare Strong Alternative Documents

If you do not have a payslip, it helps to prepare other records that demonstrate how you earn and manage your money. These could include bank statements showing regular deposits over time, your CPF contribution history, IRAS Notices of Assessment (NOA), an employment contract or offer letter, invoices, or business transaction records. The more consistent and organised your documents are, the easier it is for lenders to process your personal loan application without standard income proof in Singapore.

#2 Keep Your Debt Levels in Check

As we’ve outlined earlier, there are caps on the total amount you can borrow from all licensed money lenders in Singapore based on your annual income and residency status; it is also mandatory for lenders to review your Moneylenders Credit Bureau (MLCB) report to ascertain your repayment ability before granting any loan.

If you have existing debt obligations and are already close to your borrowing limit, approval may be more challenging. Paying down smaller debts where possible, or applying for a more manageable amount, can improve your chances of getting a loan without traditional income proof.

Choose Reliable Licensed Money Lenders Like UK Credit

The bottom line is this: getting a personal loan without payslips is possible, but success depends on your ability to demonstrate consistent income and repayment capacity. Choosing to work with trusted licensed lenders like UK Credit can protect borrowers like you and me from exploitative and illegal practices.

Ready to explore safe, legal options for personal loans without standard income proof? Submit your application online now or reach out to us for a no-obligation chat on your financial needs. We’re more than happy to be of service to you in your loan journey.